CUANMOLOGI Just another WordPress site

CUANMOLOGI Just another WordPress site

Related Articles

Are you struggling with high monthly car loan payments? Looking for ways to reduce your interest rate and save money on your auto financing? Refinancing your auto loan could be the solution you’ve been searching for. In this comprehensive guide, we will walk you through everything you need to know about refinancing your auto loan, from understanding the process to the benefits it offers. By the end of this article, you’ll be equipped with the knowledge to make an informed decision and potentially save hundreds or even thousands of dollars on your car loan.

Before we dive into the details, let’s briefly explain what refinancing an auto loan means. When you refinance your car loan, you essentially replace your existing loan with a new one, usually with better terms and conditions. This new loan pays off your current loan, and you start making payments on the new loan instead. Now, let’s explore the key aspects of refinancing your auto loan in more detail.

Understanding Auto Loan Refinancing

Refinancing an auto loan involves obtaining a new loan to replace your existing car loan. This new loan usually comes with improved terms, such as a lower interest rate, extended repayment period, or both. By refinancing, you can potentially reduce your monthly payments and save money over the life of the loan. It’s important to note that refinancing is not limited to situations where you’re struggling with your current loan; it can also be a strategic move to take advantage of better market conditions, improve your credit score, or simply secure more favorable loan terms. Let’s delve deeper into the benefits, eligibility criteria, and the potential impact on your credit score.

The Benefits of Auto Loan Refinancing

Refinancing your auto loan can offer several benefits. One of the primary advantages is the potential to secure a lower interest rate. If interest rates have dropped since you initially took out your car loan, refinancing can allow you to take advantage of the favorable market conditions and reduce the overall cost of your loan. Another benefit is the opportunity to extend the repayment period. By extending the term of your loan, you can spread out your payments over a longer period, resulting in lower monthly payments. This can be especially beneficial if you’re experiencing financial strain or if you want to free up some cash flow for other expenses. Additionally, refinancing can help you consolidate multiple loans, such as credit card debt or personal loans, into a single, more manageable payment. This can simplify your finances and potentially save you money on interest charges. Overall, the benefits of refinancing your auto loan can vary depending on your individual circumstances, but it’s crucial to consider the potential cost savings and improved loan terms.

Eligibility Criteria for Auto Loan Refinancing

Before diving into the refinancing process, it’s important to understand the eligibility criteria set by lenders. While specific requirements may vary among lenders, there are some common factors that lenders consider when assessing your eligibility for refinancing. Firstly, your credit score plays a vital role. Lenders typically prefer borrowers with good to excellent credit scores, as it demonstrates a history of responsible borrowing and increases the likelihood of repayment. A higher credit score can also lead to more favorable interest rates. Secondly, lenders review your current loan-to-value (LTV) ratio, which is the remaining balance on your car loan compared to the value of your vehicle. A lower LTV ratio indicates less risk for the lender and improves your chances of getting approved for refinancing. Additionally, lenders may consider your income, employment history, and debt-to-income ratio (DTI), which is the percentage of your monthly income that goes towards debt payments. Meeting these eligibility criteria increases your chances of getting approved for refinancing and securing better loan terms.

The Impact of Auto Loan Refinancing on Your Credit Score

One concern many borrowers have when considering refinancing their auto loan is the potential impact on their credit score. While refinancing itself does not inherently damage your credit score, certain factors associated with the process can have an impact. When you apply for refinancing, lenders will typically conduct a hard inquiry on your credit report. This inquiry can cause a temporary dip in your credit score, but its impact is usually minimal. However, regularly applying for refinancing or multiple loans within a short period can raise concerns and negatively affect your credit score. On the flip side, if you successfully refinance your auto loan and consistently make timely payments on the new loan, it can have a positive impact on your credit score over time. By reducing your debt-to-income ratio and demonstrating responsible financial behavior, you can strengthen your creditworthiness. It’s important to weigh the potential impact on your credit score against the potential benefits of refinancing before making a decision.

When to Consider Auto Loan Refinancing

Knowing when it’s the right time to refinance your auto loan can make a significant difference in your financial situation. While there’s no one-size-fits-all answer, certain signs and factors indicate that exploring refinancing options may be worthwhile. Let’s delve into these considerations to help you determine if refinancing is the right move for you.

Interest Rate Reduction

One of the most compelling reasons to consider refinancing your auto loan is the opportunity to secure a lower interest rate. If interest rates have dropped since you initially obtained your loan or if you’ve improved your creditworthiness, you may be eligible for a more favorable rate. By reducing the interest rate, you can potentially save a significant amount of money over the life of the loan. It’s worth monitoring the prevailing interest rates and comparing them to your current rate to determine if refinancing would result in substantial savings.

Improved Credit Score

If you’ve taken steps to improve your credit score since obtaining your car loan, refinancing can be a strategic move to take advantage of your improved creditworthiness. A higher credit score can open doors to better loan terms, including lower interest rates and more favorable repayment options. Before applying for refinancing, it’s advisable to check your credit score and review your credit report to ensure accuracy. If you’ve significantly improved your credit score and meet the other eligibility criteria, refinancing could be a viable option to save money on your auto loan.

Change in Financial Situation

Life is full of unexpected changes, and your financial situation may not be the same as when you initially obtained your car loan. If you’re experiencing financial strain, refinancing can potentially provide relief by lowering your monthly payments. By extending the repayment period or securing a lower interest rate, you can reduce the financial burden and free up cash flow for other essential expenses. On the other hand, if your financial situation has improved, you may consider refinancing to pay off your loan faster. By securing a shorter loan term or making higher monthly payments, you can save on interest charges and become debt-free sooner. Assessing your current financial situation is crucial in determining whether refinancing aligns with your goals and needs.

Change in Vehicle Value

The value of your vehicle can impact your chances of securing a favorable refinancing deal. If your car’s value has significantly decreased since you obtained your loan, you may find it challenging to refinance. Lenders typically consider the loan-to-value (LTV) ratio, and a higher ratio may result in less attractive loan terms or even rejection. Conversely, if your vehicle’s value has increased or remained stable, you may have a better chance of getting approved for refinancing and securing more favorable terms. Monitoring your vehicle’s value and staying informed about market trends can help you determine if refinancing is a viable option.

Early Payment Penalties

Before considering refinancing, it’s essential to review your current loan agreement for any early payment penalties. Some lenders impose penalties if you pay off your loan before a specific period. These penalties can negate the potential savings from refinancing. However, don’t let early payment penalties deter you from exploring refinancing options altogether. Calculate the potential savings from refinancing and compare them to the penalties to determine if it’s financially beneficial in the long run.

How to Find the Best Refinance Auto Loan Rates

Securing the best refinancing rates is crucial for maximizing your savings and achieving your financial goals. While finding the perfect rate may require some effort, it’s well worth the time and research. Here are some steps to guide you in finding the best refinance auto loan rates:

1. Assess Your Current Loan Terms

Before starting your search for refinancing options, evaluate your current loan terms. Review the interest rate, remaining balance, and remaining repayment period. Understanding your current loan details will help you compare potential offers more effectively and determine if refinancing is financially beneficial.

2. Research Multiple Lenders

Don’t settle for the first lender you come across. Take the time to research and compare rates from multiple lenders, including banks, credit unions, and online lenders. Each lender may have different criteria, rates, and fees, so obtaining quotes from various sources will give you a comprehensive view of the available options.

3. Check Your Credit Score

Your credit score plays a significant role in the interest rates you’re offered. Before applying for refinancing, check your credit score and review your credit report for any errors. If your score has improved since obtaining your current loan, you may be eligible for better rates. On the other hand, if your credit score has declined, it’s essential to assess whether refinancing is financiallybeneficial at this time or if you should focus on improving your credit before applying for refinancing.

4. Consider Loan Term Options

When comparing refinance auto loan rates, pay attention to the loan term options offered by different lenders. While longer loan terms may result in lower monthly payments, they can also lead to higher overall interest costs. Conversely, shorter loan terms may have higher monthly payments but can save you money on interest in the long run. Consider your financial situation and goals to determine the most suitable loan term for your needs.

5. Understand Fees and Closing Costs

Refinancing your auto loan often involves fees and closing costs. These can include application fees, origination fees, appraisal fees, and title transfer fees, among others. When comparing rates, make sure to inquire about the associated fees to understand the total cost of refinancing. Additionally, consider the impact of these fees on your potential savings and weigh them against the benefits of refinancing.

6. Negotiate with Lenders

Don’t be afraid to negotiate with lenders to secure better rates and terms. If you receive multiple offers, use them as leverage to negotiate with your preferred lender. Even a small reduction in the interest rate can result in significant savings over the life of the loan. Be prepared to provide documentation to support your negotiation, such as proof of income and credit history.

7. Consider Online Lenders

Online lenders have become increasingly popular in the auto loan refinancing market. They often offer competitive rates and convenient application processes. Consider exploring reputable online lenders to expand your options and potentially find better rates. However, exercise caution and thoroughly research each online lender to ensure their legitimacy and credibility.

8. Read Customer Reviews

Customer reviews can provide valuable insights into a lender’s reputation, customer service, and overall experience. Take the time to read reviews and testimonials from other borrowers who have refinanced their auto loans with the lenders you’re considering. These reviews can help you gauge the level of customer satisfaction and identify any potential red flags.

The Application Process for Refinancing Your Auto Loan

Ready to take the plunge and refinance your auto loan? Understanding the application process is essential for a smooth and successful refinancing experience. Below, we’ll walk you through the key steps involved:

1. Gather Necessary Documentation

Before starting the application process, gather the necessary documentation. This typically includes proof of income, such as recent pay stubs or tax returns, proof of insurance, vehicle registration, and your current loan details. Having these documents readily available will streamline the application process and help lenders assess your eligibility more efficiently.

2. Research and Select Lenders

Based on your research and comparison of rates and terms, select the lenders you wish to apply to. Consider both traditional banks and online lenders to have a comprehensive range of options. Keep in mind that applying to multiple lenders within a short period can result in multiple hard inquiries on your credit report, which may temporarily impact your credit score.

3. Complete the Application

Once you’ve selected the lenders, complete the application forms provided by each lender. Ensure that you provide accurate and up-to-date information, as any discrepancies can delay the processing of your application. Double-check the forms for completeness and review the terms and conditions before submitting.

4. Await Approval and Compare Offers

After submitting your applications, you’ll need to wait for the lenders to review and assess your eligibility. This process can take a few days to a couple of weeks, depending on the lender. Once you start receiving offers, carefully compare them, considering factors such as interest rates, loan terms, fees, and closing costs. Evaluate the total cost of refinancing and the potential savings to make an informed decision.

5. Provide Additional Documentation, if Required

In some cases, lenders may request additional documentation or clarification during the review process. Be prepared to provide any requested information promptly to avoid delays. Promptly responding to lender requests will help expedite the approval process and increase your chances of securing the desired refinancing terms.

6. Accept the Best Offer and Close the Loan

Once you’ve compared the offers and selected the best one, inform the lender of your decision. They will guide you through the closing process, which typically involves signing the necessary documents and transferring the title of your vehicle. Review the loan agreement carefully before signing to ensure you understand the terms and conditions. After closing the loan, your new lender will pay off your existing loan, and you’ll start making payments on the new loan according to the agreed-upon terms.

Pros and Cons of Refinancing Your Auto Loan

Like any financial decision, refinancing your auto loan comes with both advantages and disadvantages. Understanding the pros and cons will help you make an informed decision and determine if refinancing aligns with your financial goals. Let’s explore the various aspects:

Pros of Refinancing Your Auto Loan

- Lower Interest Rates: One of the primary benefits of refinancing is the potential to secure a lower interest rate, which can lead to significant cost savings over the life of the loan.

- Reduced Monthly Payments: By extending the loan term or securing a lower interest rate, refinancing can help lower your monthly payments, providing immediate financial relief.

- Improved Loan Terms: Refinancing allows you to modify the terms of your loan, such as the repayment period, allowing you to align the loan with your current financial situation and goals.

- Consolidation of Debt: If you have multiple debts, refinancing your auto loan can provide an opportunity to consolidate them into a single loan, simplifying your financial obligations.

- Improved Credit Score: Consistently making payments on your refinanced auto loan can positively impact your credit score, demonstrating responsible financial behavior and improving your creditworthiness.

Cons of Refinancing Your Auto Loan

- Extended Repayment Period: While extending the loan term can lower your monthly payments, it can also result in higher overall interest costs and a longer time to pay off the debt.

- Additional Fees and Costs: Refinancing your auto loan may involve fees and closing costs, which can eat into the potential savings. It’s important to consider these costs and weigh them against the benefits.

- Hard Inquiry on Credit Report: When you apply for refinancing, lenders typically conduct a hard inquiry on your credit report, which can temporarily lower your credit score. Multiple hard inquiries within a short period can have a more significant impact.

- Possibility of Prepayment Penalties: Some lenders impose prepayment penalties if you pay off your loan before a specific period. These penalties can outweigh the potential savings from refinancing, making it less financially advantageous.

- Not Suitable for All Situations: Refinancing may not be the best option for everyone. If you’re nearing the end of your loan term or if your vehicle’s value has significantly depreciated, the potential benefits may not outweigh the costs and effort involved.

Understanding Auto Loan Refinance Fees and Costs

While refinancing can save you money in the long run, it’s essential to be aware of the fees and costs associated with the process. These fees can vary depending on the lender and your specific circumstances. Let’s explore the common fees and costs you may encounter when refinancing your auto loan:

Application Fees

Some lenders charge an application fee when you apply for refinancing. This fee covers the administrative costs associated with reviewing your application and assessing your eligibility. Application fees can range from a nominal amount to a percentage of the loan amount, so it’s important to inquire about this fee upfront.

Origination Fees

Origination fees are charged by lenders to cover the costs of processing your loan. These fees are typically a percentage of the loan amount and can vary among lenders. Origination fees can significantly impact the total cost of refinancing, so it’s crucial to consider them when comparing offers.

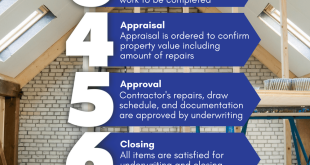

Appraisal Fees

In some cases, lenders may require an appraisal of your vehicle to determine its value before approving your refinancing application. The appraisal fee covers the cost of assessing your vehicle’s worth. While not all lenders require an appraisal, it’s important to factor in this potential cost when considering refinancing.

Title Transfer Fees

When refinancing your auto loan, the new lender will require the title of your vehicle to be transferred to their name as collateral. This transfer of title incurs a fee, which covers the administrative costs associated with updating the ownership records. Title transfer fees can vary depending on your location and the specific requirements of the lender.

Prepayment Penalties

Prepayment penalties are charges imposed by some lenders if you pay off your loan before a specific period. These penalties are designed to compensate the lender for the potential loss of interest income. It’s essential to review your current loan agreement for any prepayment penalties before deciding to refinance. If your current loan has prepayment penalties, carefully consider whether the potential savings from refinancing outweigh the cost of these penalties.

Other Potential Costs

In addition to the fees mentioned above, there may be other potential costs associated with refinancing your auto loan. These can include document processing fees, notary fees, and state or local taxes. It’s important to inquire about any additional costs that may apply and factor them into your decision-making process.

When comparing refinancing offers, consider the total cost of refinancing, including all fees and costs associated with the loan. While securing a lower interest rate is often a primary goal, it’s crucial to evaluate the potential savings in relation to the fees and costs involved. Carefully review the loan agreement and ask the lender for clarification on any fees or costs that are not clearly disclosed.

How Refinancing Can Improve Your Credit Score

Curious about the impact of refinancing your auto loan on your credit score? While refinancing itself does not inherently boost your credit score, it can indirectly contribute to improving your creditworthiness. Here’s how refinancing can potentially positively impact your credit score:

Lower Debt-to-Income Ratio

Refinancing your auto loan can potentially lower your debt-to-income (DTI) ratio, which is the percentage of your monthly income that goes toward debt payments. By securing a lower interest rate or extending the loan term, you can reduce your monthly payments, effectively lowering your DTI ratio. A lower DTI ratio is generally viewed favorably by lenders and can contribute to an improved credit score.

Timely Payments on the New Loan

Consistently making timely payments on your refinanced auto loan is crucial for improving your credit score. Payment history is one of the most significant factors influencing your credit score, so ensuring that you make on-time payments each month demonstrates responsible financial behavior. Over time, this positive payment history can contribute to a higher credit score.

Diversification of Credit

Refinancing your auto loan can also contribute to diversifying your credit mix. Credit mix refers to the different types of credit you have, such as credit cards, mortgages, and auto loans. Having a diverse credit mix is generally viewed positively by credit bureaus and can potentially boost your credit score. By adding an auto loan refinancing to your credit mix, you can demonstrate your ability to manage different types of credit responsibly.

Reduced Credit Utilization

If you use the savings from refinancing to pay down other debts, such as credit card balances, it can lower your overall credit utilization ratio. Credit utilization ratio is the percentage of your available credit that you’re using and is an important factor in determining your credit score. By reducing your credit utilization, you can potentially improve your credit score.

It’s important to note that the impact on your credit score may vary depending on your individual circumstances and credit history. While refinancing can offer potential benefits, it’s crucial to continue practicing responsible financial habits, such as making timely payments and managing your credit wisely, to maintain and improve your credit score over time.

Alternatives to Auto Loan Refinancing

Refinancing your auto loan may not always be the best option for everyone. Depending on your financial situation and goals, there may be alternative strategies to consider. Here are a few alternatives to auto loan refinancing:

Loan Modifications

If you’re struggling with your current auto loan payments, contacting your lender to explore loan modification options can be a viable alternative. Loan modifications involve negotiating with your lender to adjust the terms of your loan. This can include extending the loan term, reducing the interest rate, or temporarily lowering the monthly payments. Loan modifications can provide immediate relief and help you avoid the costs and process of refinancing.

Extend the Loan Term

If your primary goal is to lower your monthly payments, extending the loan term on your current auto loan may be an option to consider. By extending the repayment period, you can spread out your payments over a longer period, resulting in lower monthly payments. However, keep in mind that extending the loan term can increase the overall interest costs, so carefully weigh the potential savings against the long-term impact on your finances.

Pay Off the Loan Early

If you’re in a more favorable financial position and want to save on interest costs, paying off your auto loan early can be a proactive strategy. By making larger or additional payments toward your principal balance, you can reduce the overall interest charges and become debt-free sooner. Before implementing this strategy, review your loan agreement for any prepayment penalties and ensure that you have the financial means to make extra payments without straining your budget.

Explore Other Financing Options

Depending on your goals and financial situation, exploring other financing options may be worth considering. This could involve seeking a personal loan with a lower interest rate to pay off your auto loan, utilizing a home equity loan or line of credit if you own property, or even considering a balance transfer to a credit card with a promotional 0% interest rate. Each option has its own pros and cons, so carefully evaluate the terms and consider the potential impact on your overall financial situation before proceeding.

Tips for a Smooth Auto Loan Refinancing Journey

Refinancing your auto loan can be a complex process, but with the right approach, it can be hassle-free. Here are some valuable tips to ensure a smooth auto loan refinancing journey:

1. Review Your Credit Reports

Prior to applying for refinancing, review your credit reports from all three major credit bureaus (Experian, Equifax, and TransUnion). Check for any errors or discrepancies that may impact your creditworthiness. Dispute any inaccuracies and ensure that your credit reports reflect an accurate representation of your credit history.

2. Improve Your Credit Score, if Possible

If your credit score is less than ideal, take steps to improve it before applying for refinancing. Pay down credit card balances, make all payments on time, and avoid applying for new credit in the months leading up to refinancing. A higher credit score can help you secure better rates and terms.

3. Gather All Necessary Documentation

Collect all the necessary documentation, including proof of income, vehicle registration, insurance information, and your current loan details. Having this information readily available will expedite the application process and help lenders assess your eligibility more efficiently.

4. Shop Around and Compare Offers

Don’t settle for the first refinancing offer you receive. Shop around and compare rates, terms, and fees from multiple lenders. Use online comparison tools, consult with local banks or credit unions, and consider reputable online lenders to expand your options. Comparing offers will help you secure the most favorable terms.

5. Understand the Total Cost of Refinancing

When comparing offers, consider the total cost of refinancing, including interest rates, fees, and closing costs. Calculate the potential savings over the life of the loan and weigh them against the costs involved. This comprehensive assessment will help you make an informed decision.

6. Communicate and Negotiate with Lenders

Don’t hesitate to communicate with lenders and negotiate for better rates and terms. If you receive multiple offers, use them as leverage to negotiate with your preferred lender. Even a slight reduction in the interest rate can result in significant savings over time. Be prepared to provide documentation to support your negotiation.

7. Read and Understand the Loan Agreement

Before signing any loan agreement, carefully read and understand the terms and conditions. Pay attention to the interest rate, loan term, fees, and any prepayment penalties. Seek clarification from the lender if you have any questions or concerns. Ensure that you are comfortable with the terms before proceeding.

8. Make Timely Payments on the New Loan

Once you’ve successfully refinanced your auto loan, it’s crucial to make all payments on time. Timely payments not only help you avoid late fees and penalties but also contribute to improving your credit score. Set up automatic payments or reminders to ensure that you never miss a payment.

Frequently Asked Questions about Auto Loan Refinancing

Still have some burning questions about refinancing your auto loan? Here are answers to frequently asked questions to clear any remaining doubts you may have:

Q: Is it worth refinancing my auto loan?

A: Whether refinancing is worth it depends on various factors, such as your current interest rate, credit score, and financial goals. By securing a lower interest rate or better loan terms, refinancing can potentially save you money over the life of the loan. However, it’s essential to consider the associated fees and costs and weigh them against the potential savings.

Q: Can I refinance my auto loan if I have bad credit?

A: While having bad credit can make refinancing more challenging, it’s not impossible. Some lenders specialize in working with borrowers with less-than-perfect credit. However, expect higher interest rates and more stringent eligibility criteria. It’s advisable to improve your credit score before applying for refinancing to increase your chances of securing better rates.

Q: Can I refinance ifI have negative equity on my car loan?

A: Refinancing with negative equity, also known as being “upside down” on your car loan, can be challenging but not impossible. Negative equity occurs when the value of your vehicle is less than the outstanding balance on your loan. In such cases, lenders may require you to pay off the negative equity upfront or include it in the new loan. It’s important to carefully evaluate the potential costs and savings before proceeding with refinancing.

Q: Can I refinance my auto loan if I’ve missed payments?

A: Missing payments on your current auto loan can negatively impact your credit score and make it more difficult to refinance. Lenders typically prefer borrowers with a history of timely payments. However, some lenders may still consider your application if you can demonstrate that the missed payments were due to temporary financial hardships. It’s important to communicate with potential lenders and provide an explanation for any missed payments.

Q: How long does the auto loan refinancing process take?

A: The auto loan refinancing process can vary in duration depending on several factors, including the lender’s processing time and the completeness of your application. On average, the process can take anywhere from a few days to a couple of weeks. It’s important to stay in touch with the lender, promptly provide any requested documentation, and be prepared for potential delays.

Q: Can I refinance my auto loan multiple times?

A: Yes, it is possible to refinance your auto loan multiple times, but it’s important to consider the potential impact on your credit score and the costs involved. Each time you refinance, you’ll likely incur fees and undergo a credit inquiry, which can temporarily lower your credit score. It’s advisable to carefully evaluate the potential benefits and costs before deciding to refinance multiple times.

Q: Will refinancing my auto loan affect my insurance?

A: Refinancing your auto loan typically does not directly impact your insurance. However, it’s important to notify your insurance provider of any changes in the loan terms, such as the lender or the loan amount. Some lenders may have specific insurance requirements, such as maintaining certain coverage levels, which you need to communicate to your insurance provider.

Q: Can I refinance an auto loan that is already at a low interest rate?

A: Refinancing an auto loan that already has a low interest rate may not always result in significant savings. However, if you’re looking to modify other aspects of the loan, such as the loan term or monthly payments, refinancing may still be worth considering. It’s important to carefully evaluate the potential costs and savings before making a decision.

By considering these frequently asked questions, you can find additional clarity and make an informed decision about refinancing your auto loan.

In conclusion, refinancing your auto loan can be a game-changer when it comes to saving money and improving your financial well-being. By understanding the process, knowing when to consider refinancing, and exploring the best rates and terms, you can take control of your car loan and potentially reduce your monthly payments. Remember to weigh the pros and cons, consider alternative options, and always make an informed decision based on your unique circumstances. Start exploring your refinancing options today and pave the way for a financially secure future.